Pending Ratios & Inventory—Your Spring Market Playbook

Ryan Cook Published on: 16/02/2026

Ryan Cook Published on: 16/02/2026Use pending ratios and inventory data to guide client strategies, set pricing, and create standout social posts in the MA/RI spring market.

Ryan Cook Published on: 16/02/2026

Ryan Cook Published on: 16/02/2026Use pending ratios and inventory data to guide client strategies, set pricing, and create standout social posts in the MA/RI spring market.

Ryan Cook

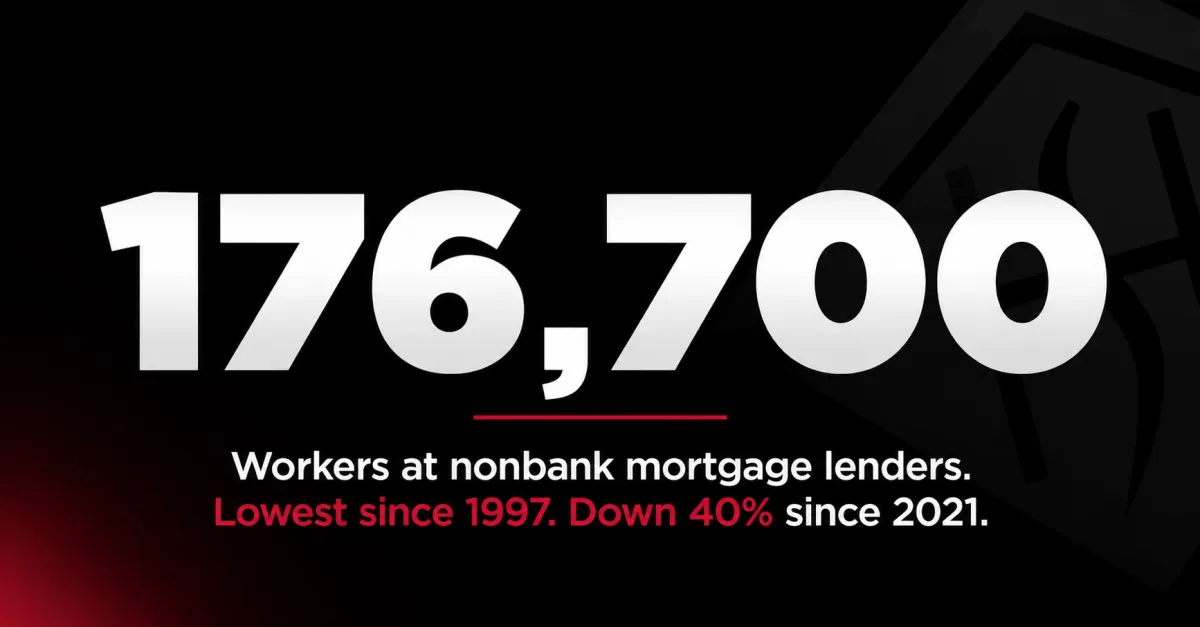

Ryan CookMortgage lender jobs hit lowest since 1997—MA & RI agents must rethink buyer financing advice.

Ryan Cook

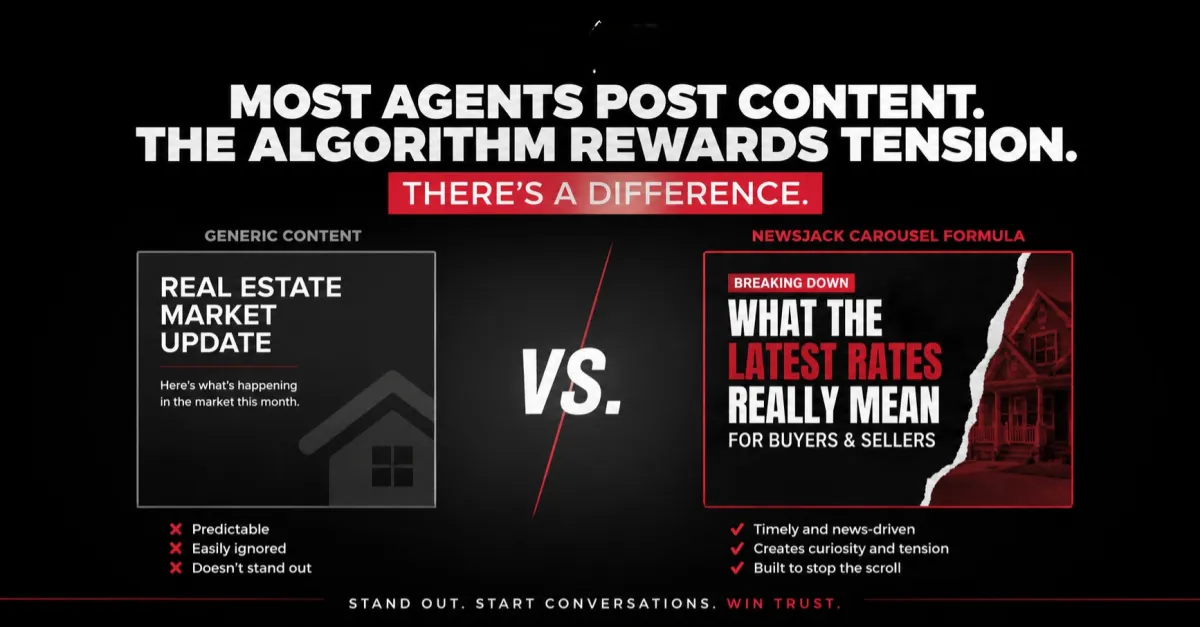

Ryan CookReal estate agents lose on social media by posting content that doesn’t stop the scroll.

Ryan Cook

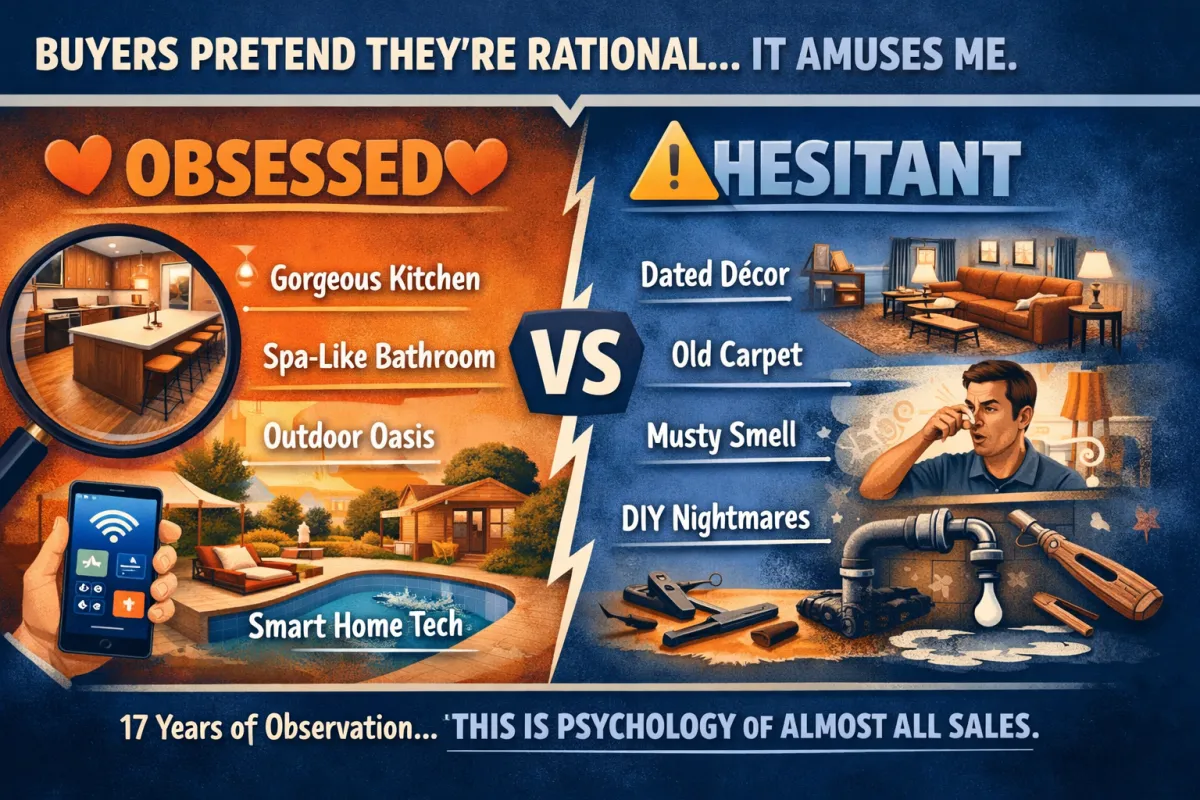

Ryan CookBuyers aren’t rational—they’re emotional first. Here are the small home features that create obsession (mudrooms, pantries, usable yards) and the ones that trigger hesitation (over-custom built-ins, bad flow, trendy “luxury”).

Ryan Cook

Ryan CookA simple Providence night plan: start at The Royal Bobcat, commit to dinner at Massimo, and finish with espresso and dessert at Pastiche. Three stops, 90 minutes, no overthinking.