The Hidden Cost of Waiting for Rates to Drop

The Comfortable Lie Buyers Keep Telling Themselves

“We’re waiting for rates to drop.”

That sounds prudent. Disciplined. Mature. Like you’re the only adult in the room while everyone else is panic-buying granite countertops and pretending beige vinyl siding is “charming.”

But most people saying that are not following a strategy. They’re hiding inside a headline.

Because “waiting for rates” only works if lower rates arrive before higher prices, tighter competition, and bigger cash requirements wipe out the benefit. And in the real world, that is not how this usually plays out.

Let’s do a little math to show you what it means.

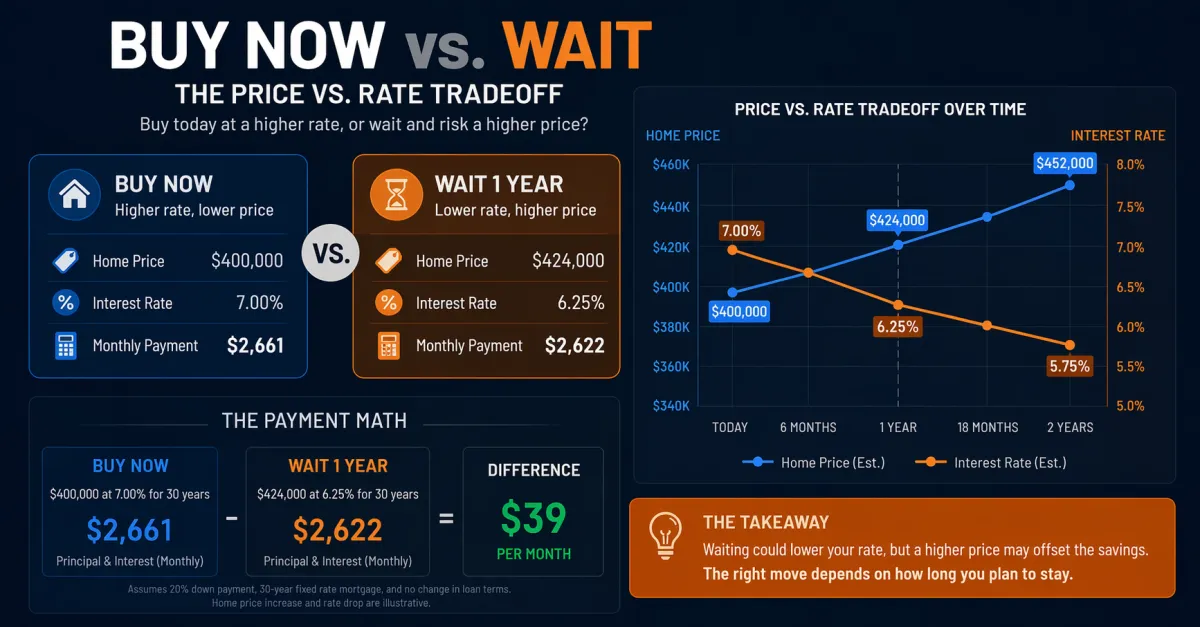

The Math Most People Conveniently Avoid

Let’s start with a simple example.

Say you could buy a $650,000 home today with 20% down.

Purchase price: $650,000

Down payment: $130,000

Loan amount: $520,000

Interest rate: 6.75%

Monthly principal and interest: about $3,372

Now let’s say you wait. Rates improve to 5.875%. Great, right? Champagne for everybody. CNBC gets excited. CNN still finds a way to spin it like President Trump is ruining your life. Your cousin, who got a license 5 years ago and has never sold a single home, suddenly becomes a housing economist.

But now that same house — or the market segment you were shopping in — costs $705,000.

Purchase price: $705,000

Down payment: $141,000

Loan amount: $564,000

Interest rate: 5.875%

Monthly principal and interest: about $3,336

So what did waiting buy you?

Monthly savings: about $36 🥳

Extra cash needed upfront: $11,000 😩

Higher purchase price: $55,000 😯

That’s not some brilliant market hack. You cost yourself $66,000 to save $36! Just some simple math… 36 goes into 66,000 about 1,833x.

You don’t need a college degree in math or engineering to know that THAT math doesn’t math.

The “Rate Drop” Fantasy Falls Apart Fast

This is the part people miss: a lower rate helps the payment, but a higher price attacks everything else.

A higher purchase price means:

a larger down payment

a larger loan balance

higher closing costs in many cases

higher property taxes over time

more money tied up just to get in the door

So even if the payment comes out close, the buyer often had to bring in meaningfully more cash to achieve that “win.”

That is not nothing. Especially for buyers who are already stretching.

What If Prices Rise Even More?

Now let’s make it less comfortable.

If that $650,000 house rises by 10%, it becomes $715,000.

At 20% down, that means:

Down payment rises from $130,000 to $143,000 (⬆️ $13,000)

Loan amount rises from $520,000 to $572,000 (⬆️ $52,000)

Even with a lower rate, you are now trying to offset a much larger loan with a modest financing improvement. That is like bragging that you saved $100 because you spent $10,000!

The question is not simply, “Did rates improve?”

The question is:

Did rates improve enough to overcome the higher price?

Usually, the answer is: not by as much as people assume.

The Break-Even Question Nobody Asks

Here’s the only question that matters:

How far do rates need to fall to offset the increase in price?

Because if prices rise 5% to 10% while you wait, rates do not just need to come down a little. They need to come down enough to neutralize:

the bigger loan

the bigger down payment

the stronger competition

the weaker negotiating leverage

And that last part matters more than the spreadsheets.

The Competition Tax Is Real

If rates fall meaningfully, buyers come back with a vengeance. This is why I’ve been against the rate drops. Keeps the rates where they are and suck all of the excess money out of the economy. Let inflation drop to 0%.

Because every rate drop pushes more money into the economy further driving up prices.

That’s not theory. We’ve already seen it multiple times. The Supply & Demand curve isn’t a theory – it’s the law!

More showings. More urgency. More multiple-offer situations. More buyers suddenly deciding they are “ready.” More sellers getting bolder. Fewer concessions. Less flexibility. More emotional bidding.

So even if lower rates improve the monthly payment on paper, the market often claws that benefit right back through competition.

That means the cost of waiting is not just measured in dollars. It is also measured in:

houses you lose

inspections you feel pressured to waive (at least in RI, not in MA, where it’s now illegal to offer to waive an inspection for anything other than new construction homes)

concessions you no longer get

decisions you make faster and under more stress

People love to talk about the payment. They almost never talk about the terms.

That’s a mistake and a rookie move.

Why Waiting Keeps Failing as a “Strategy”

Waiting is not automatically wrong. Blind waiting is.

If your plan is:

“I’ll sit here until rates drop, and then somehow prices will also be better, inventory will be better, and competition will be calmer...”

That is not a strategy. That is wishful thinking with a mortgage podcast playing in the background.

The market does not reward people for sounding cautious. It may reward people for broadcasting caution… but reality rewards people who understand tradeoffs.

The Smarter Question to Ask

Instead of asking:

“Should I wait for rates?”

ask:

“If the right house showed up now, could I afford the payment... and what exactly do I believe will be better later?”

Better price? Maybe not.

Better competition? Probably not.

Better inventory? Not guaranteed.

Better payment? Possibly... but not always enough to matter once the rest shifts against you.

Bottom Line

A lower mortgage rate can absolutely help.

But if prices rise while you wait — and if demand wakes up the second rates soften — your reward for “being patient” may be a slightly lower rate attached to a more expensive house, a larger down payment, and a more competitive market.

It’s exactly what I’ve seen for the last 6 years.