Mortgage Rates in Times of Conflict: What History Tells Us About Today’s Market

Mortgage Rates in Times of Conflict: What History Tells Us About Today’s Market

Introduction: Are Today’s Low Rates Here to Stay?

Mortgage rates have dropped to their lowest point since 2022, just as new international tensions in the Middle East, and even Ecuador, are making headlines.

The new Fed chief has suggested additional rate cuts in 2026 yet I’m skeptical.

Since history has a way of repeating itself, I want to understand one thing: How will this affect rates and does history suggest this dip is an opportunity, or a mirage?

The Historical Dance: Conflict, Uncertainty, and Mortgage Rates

Periods of U.S. involvement in global conflict have repeatedly triggered sharp reactions in the mortgage market. When the Gulf War began in 1990, investors rushed to safe assets, pushing 30-year fixed rates from around 10% to the low 9% range. After 9/11, rates fell swiftly as the Federal Reserve slashed rates to stabilize the economy. The 2022 Ukraine-Russia crisis played out similarly—initial panic drove rates down, but inflation and energy shocks soon sent them soaring to multi-year highs.

Mortgage Rates and Key Conflicts

, the Afghanistan/Iraq wars (2001-03), the Ukraine/Russia conflict (2022), and a hypothetical scenario \"Current (2026)\". The columns present the Conflict/Event, Year(s), the start of the 30-Year Rate, the rate 6 months later, Unemployment, and the Inflation Trend. For each event, the table displays the specific percentages for the 30-year interest rates and their trends, the corresponding changes in unemployment rates, and a qualitative description of the inflation during that period. For the \"Current (2026)\" entry, the 30-Year Rate Start is 5.1%, the 6 Months Later value is TBD, Unemployment is Stable/↓, and the Inflation Trend is Cooling inflation.")

NOTE: It was difficult to pull this information together manually, so I asked AI to help pull the data and put it into a chart and it produced the above chart… hence the funky spellings.

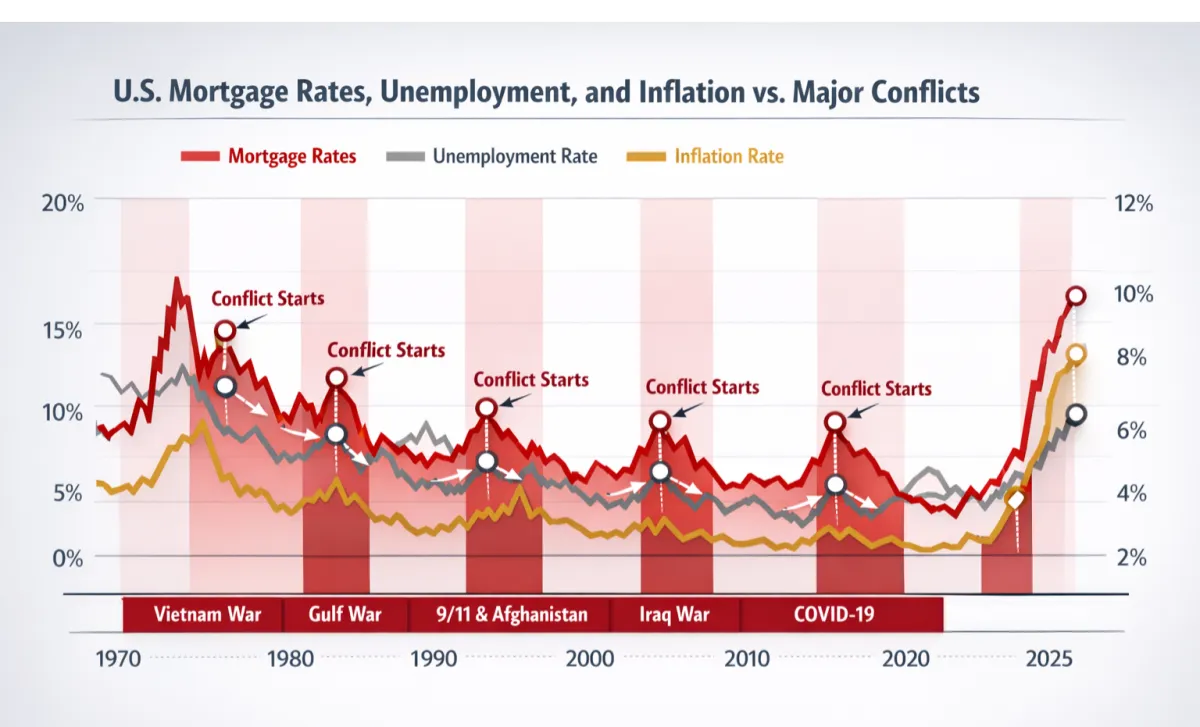

Visual Analysis: What the Chart Reveals

The timeline chart above shows how mortgage rates, unemployment, and inflation have moved together in the U.S. over the past few decades, especially during times of international conflict… which is what we’re exploring here.

Each shaded area marks a major event—like the Gulf War, the wars in Afghanistan and Iraq, and the Ukraine/Russia crisis—so you can see what happened to the economy when uncertainty spiked.

I noticed two things right away and it depends on WHEN we are in the conflict.

When a conflict begins, you’ll notice the following:

Mortgage rates often drop quickly as investors seek safety and the government or Federal Reserve steps in to stabilize things.

Unemployment may tick up or remain steady at first.

Inflation can stay quiet or begin to rise.

As the conflict wears on, things tend to shift… and I need to reorder the above so you can see the connection:

Inflation tends to climb as supply chains are disrupted or government spending increases.

Mortgage rates usually follow that upward trend.

Unemployment can lag behind, sometimes rising later if the broader economy slows.

The big takeaway? While it’s common to see mortgage rates dip at the start of a crisis, these drops are usually temporary. Once inflation starts to build or the economic impact of the conflict spreads, rates often rebound— sometimes even higher than before.

That’s definitely NOT what I wanted to see.

For anyone thinking about buying a home or refinancing, the lesson is to act quickly during these brief windows, but also to watch the broader economic signals. The chart makes it clear: history shows that today’s low rates may not last long if inflation or unemployment start to shift upward.

Beyond the Headlines: What Drives These Cycles?

The immediate “flight to safety” that lowers rates in times of crisis is almost always followed by a second act. As conflicts drag on, inflationary pressures—whether from government spending, supply chain disruption, or energy price spikes—tend to reverse the initial dip.

The mortgage market, in other words, is not simply reactive, but cyclical and deeply tied to macroeconomic fundamentals. It’s not always easy to spot, and it’s typically only seen in hindsight.

What Makes 2026 Different?

Today’s market is faster and more sensitive to policy than ever before. A tweet on X or a truth on Truth Social can zip across the globe at the speed of light and markets can respond instantly.

It also means the Federal Reserve (which is neither Federal nor Reserve… but that’s a diatribe for another day) can intervene in real time.

While rates have dipped again as global uncertainty rises, the underlying drivers—job market health, cost of living, and especially inflation—will determine if this window lasts.

Right now, the U.S. job market, while still strong by historical standards, is showing its first real signs of cooling. The latest Bureau of Labor Statistics report surprised many economists with weaker-than-expected job creation and a slight uptick in unemployment, now just above 4%. While layoffs remain limited and sectors like healthcare and tech are still adding positions, the overall pace of hiring has slowed more noticeably than at any point since the post-pandemic recovery began.

Wage growth—which had been outpacing inflation—is starting to flatten, raising questions about whether consumer spending power will hold up through the spring. For agents and buyers, this shift signals a market at an inflection point: confidence remains, but the risk of a softer labor market is rising. That’s not what any agent, or home seller, wants to hear.

On the cost-of-living front, the rapid increases seen during 2022–2023 have eased, but expenses—especially for housing, insurance, and utilities—remain elevated compared to pre-pandemic levels. Energy and grocery prices have stabilized somewhat, but rents and home prices are still high in most major markets, and medical costs and insurance premiums continue to pressure many families. While cost-of-living growth has slowed, affordability remains a top challenge, particularly for first-time buyers… who’ve all but been shut out of the housing market in the last few years, especially in our area.

After peaking sharply in 2022, inflation has steadily cooled, with year-over-year CPI increases now running in the 2.3–2.7% range (close to the Federal Reserve’s target). Stabilized energy prices, improved supply chains, and slower growth in goods prices have been the main drivers of this moderation.

However, “core” inflation (excluding food and energy) remains a bit stickier, especially for services and shelter. Inflation is back under control for now, but with the job market showing cracks, the Fed is likely to remain cautious—any new shocks (like international conflict or supply chain disruptions) could quickly change the outlook.

Agent Analysis: How to Guide Clients Through Uncertainty

History teaches us that rate drops during conflict are rarely permanent. The true risk is not missing a lower rate, but failing to anticipate how quickly conditions can change. Agents who can tell this story—using charts, timelines, and deep data—offer clients real insight, not just reassurance.

Conclusion: Seeing the Patterns, Acting with Confidence

The lesson is clear: In times of conflict, mortgage rates may fall, but the forces of inflation and policy response are never far behind. Those who understand the deeper cycles—grounded in data, not headlines—will be best positioned to help clients make confident, timely decisions.