The Mortgage Industry Just Hit a 29-Year Low. Here’s What That Means for Every Buyer You’re Working With.

The Mortgage Industry Just Hit a 29-Year Low. Here's What That Means for Every Buyer You're Working With.

Most agents, and buyers, are watching the mortgage rate right now hoping that the magical Federal Reserve will sprinkle some pixie dust on the real estate industry and make inventory appear out of thin air.

The only problem is that it’s the wrong number to be watching.

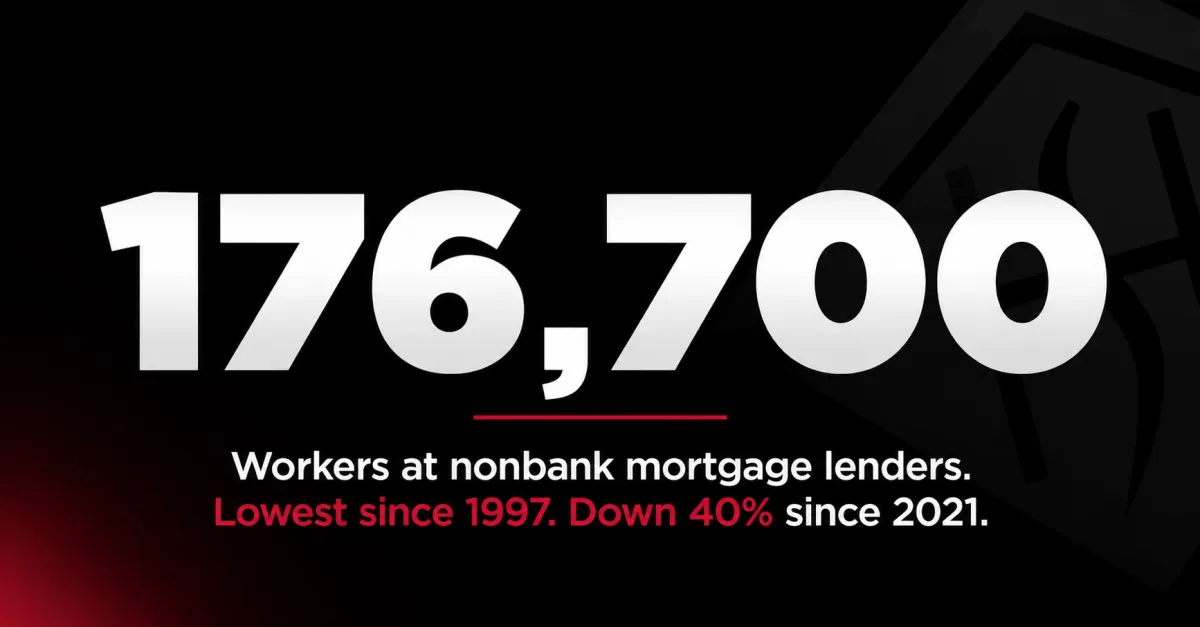

The number worth watching — the one that tells you what buyers are actually going to experience when they try to close a loan — is 176,700. That is the current count of workers employed at nonbank mortgage lenders across the United States, according to the Bureau of Labor Statistics. It is the lowest staffing level the industry has seen since 1997. And it is 40% below where it stood at the peak of the market in mid-2021.

You may not understand it… but this has consequences for every transaction you're working on right now, and most agents have no idea it happened.

Here's what you need to understand — and what you need to be able to say to the people sitting across from you.

The industry gutted itself. Twice.

What the Bureau of Labor Statistics data documents is that the mortgage industry has now lived through two employment collapses — one after the 2008 housing crash, and one playing out in slow motion since 2021. The first collapse was catastrophic. The second has been quieter, spread across four years of suppressed volume, but the math… is brutal: four out of every ten jobs that existed at the peak of the last cycle no longer exist.

Mortgage brokers — the independent professionals who shop loans across multiple lenders — shed 38% of their workforce over the same period. The industry didn't just trim. It rebuilt itself at a fraction of its previous size.

A portion of that reduction is technological. Since 2008, automation has absorbed work that used to require human processors — document handling, verification, underwriting queues.

The industry needs fewer bodies to close the same number of loans than it did twenty years ago. That is a real and legitimate shift. But it doesn't explain a 40% drop.

Volume collapsed, and the workforce followed. The lenders saw it coming — mass layoffs began in the second half of 2021, even while home prices were still climbing. The origination business was already drying up before the headlines caught on.

Why agents should care: your buyer's experience is being shaped by this.

When loan volume collapsed, lenders didn't just cut entry-level staff. They cut loan officers, processors, and underwriters — the people who sit at the center of your transactions. The survivors are the most experienced, the most efficient, and the most adaptable. But there are far fewer of them.

It means the lender your buyer calls isn't just evaluating their credit and income. That lender is handling a workload that used to be distributed across a much larger team. Processing times that feel unpredictable aren't always a sign of incompetence — they're sometimes a sign of a skeleton crew.

The agents who understand this are already doing something different. They're not sending buyers to whoever offers the lowest advertised rate. They're sending buyers to lenders and loan officers they know personally — people they've watched close deals under pressure, who communicate, who deliver what they promise. In a thin-staffed market, relationships are not a soft advantage. The right lending partner IS a closing strategy.

Does this mean less choice for your buyers?

Yes.

The nonbank lenders that dominate the US mortgage market (companies like Rocket, United Wholesale, PennyMac, loanDepot, Guaranteed Rate, and others) have collectively reduced capacity. When a buyer shops five lenders, they may be shopping five different faces of the same constrained infrastructure.

The variation in rates exists. The variation in service quality and execution reliability is often what determines whether a deal closes on time… so who you work with matters.

For buyers with complexity — self-employed income, investment properties, non-warrantable condos, recent job changes — the thinning of experienced staff matters more.

The loan officers who knew how to structure a difficult file are the ones who left or were let go when volume dried up. The ones still in seats are good. But there are fewer of them, and the complex files now compete for their attention.

What happens next depends almost entirely on rates.

The mortgage employment story has three possible chapters from here, and which one plays out changes what your next twelve months look like as an agent.

If rates drop meaningfully — even a half-point sustained decline — demand will skyrocket. Buyers who have been sitting on the sidelines since 2022 will rush back in. You know it. I know it. Heck, the buyers out there know it, too.

The problem is that the industry is running on 1997 staffing levels. A demand spike into a skeleton infrastructure will create exactly what nobody wants: long processing timelines, frustrated buyers, deal timelines that blow up, and lenders scrambling to rehire and retrain people they let go two years ago. A rate drop is good news for volume but probably not good news for your transactions in the short term.

If rates stay flat, the current environment will be more of the same. Volume stays suppressed. Lenders continue to operate lean. The market moves slowly, but predictably. Experienced loan officers have capacity, and the buyers who do transact get more attention than they did at peak.

If rates rise from here, the deep freeze deepens. Volume falls further, more capacity leaves the industry, and the gap between what the market could do and what it's actually doing gets wider. Fewer transactions, more competition for listings, and buyers with even less urgency.

The takeaway for your conversations:

When a client asks you why everything feels so slow, or why their lender seems overwhelmed, or why rates aren't dropping fast enough — you now have an answer.

The mortgage industry has contracted to its smallest workforce in nearly thirty years. That is a direct reflection of how frozen transaction volume has been since 2022. It also means the people still doing this work are carrying more than they used to, and the margin for error on lender selection is smaller than it's been in a long time. Choose wisely!

Your job is not to pick their lender. However, if you do have a strong lender you’ve been working with for a long time… it may be in your client’s best interest to take your advice, even if the rate is a little more than they’re finding on bankrate.com or Lending Tree.com.

The experienced loan officer who answers the phone, knows your market, and has closed deals in this environment is not interchangeable with whoever offers 0.125% less. In a 29-year employment low, that difference will likely be the difference between a closed deal and a dead one.